Hello all! Cohen Battisti, Attorneys at Law has transitioned its blog from WordPress to our new website. Don’t worry! We’ll have the same great legal content, but in a shiny new place. We will still post some stuff here from time to time, but the majority of our content will be on our new blog. Check out ItsAboutJustice.Law on our new site! We’ll see you there!

Author Archives: Harvey V. Cohen

Family Law 101- Attend Our Family Law Workshop January 21, 2014

Going through a divorce can be a tough experience. You are not alone! Cohen Battisti, Attorneys at Law is here to help you. Join us at our free workshop covering what you need to know about Family Law. Light hor d’oeuvres will be provided.

Start off 2014 on the right foot and have your family law questions answered.

“Partial Assignments” can be Fatal for Restoration Contractors’ Attempts to Collect Insurance Payments, and Increase Liability for Insureds

Homeowners and restoration contractors who attempt to enter into a partial assignment of insurance benefits should know that partial assignments for the contractor’s services have repeatedly been found to be invalid contracts in Florida courts. An invalid assignment contract typically results in the homeowner remaining 100% responsible for paying the contractor for the services performed on the home. This is because the insurance company is not required to honor true partial assignments and courts will not enforce an invalid contract.

Sometimes insurance companies will say that a valid, complete assignment is just a “partial assignment” because the insurance company thinks both the policyholder and the contractor are trying to collect payment for the services the contractor performed. However, this is not what either the policyholder or the contractor intended in the assignment of benefits. Once the policyholder assigns the rights and benefits to the contractor to allow direct billing and collect payment for the services the contractor performed, the policyholder no longer has any rights or interest in collecting payment for services performed by that contractor. The policyholder transferred those rights and interests to the contractor, so only the contractor is entitled to collect insurance payment for their invoice.

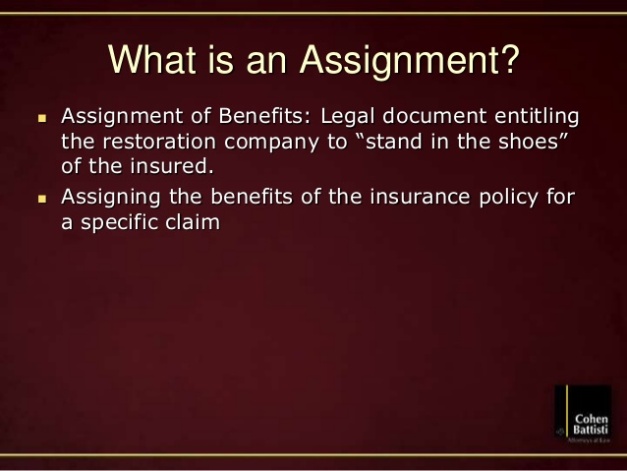

The assignment of benefits should state that the policyholder assigns and transfers “any and all insurance rights, benefits and proceeds under any applicable insurance policy” to the restoration contractor. It should be clear that the policyholder has made a complete assignment of benefits to the contractor and not a partial assignment. This is because Florida courts have held that only one entity “owns” the cause of action against an insurer at any one time and the one that owns the claim must bring the action if an action is to be brought. The reasoning is that in the case of a partial assignment, if both the policyholder and the contractor own the rights to collect payment for the contractor’s services, the insurance company is subject to multiple suits or claims for the same amount due.

Slide from Cohen Battisti’s “Insider Secrets” Slideshow

In a typical property damage insurance claim where a policyholder hires a contractor, the policyholder may assign and transfer the rights and benefits to collect payment for its services to the contractor in exchange for the contractor not requiring immediate payment from the policyholder at the time services are provided. The policyholder still remains responsible for amounts owed that the insurance company does not pay in benefits. Once the assignment takes place, the contractor owns the claim only for the value of the services they performed, and has the policyholder’s permission to directly bill the insurance company for payment of these services.

If an insurance company does not issue full payment to the contractor for its services performed after receiving a proper assignment of benefits and the contractor’s invoice, and after certain conditions are met, the contractor can proceed to collect payment directly from the insurance carrier, and if that fails, then to file suit against the insurance company.

The bottom line is that with a complete assignment of insurance benefits given to a contractor for collecting payment for services they performed, the contractor is the only owner of the claim for their services rendered. It is important to avoid partial assignments because it may not be found valid and may not be enforced in a court of law. Moreover, with a complete assignment given to a contractor for services rendered, the policyholder still, always maintains the rights to collect benefits for any damages they have which are not related to the contractor’s services performed. The list is long but can for example include payments for additional or supplemental property damage that needs repairs in the same claim, or for additional living expenses.

If you have any questions about an Assignment of Benefits or partial assignments, consult a licensed Florida attorney. At Cohen Battisti, we handle these assignment issues every day regarding insurance disputes and want to help you get paid.

Florida Enjoys 8th Year with No Hurricanes, but no Break for Homeowners Insurance

Florida has survived some of the biggest hurricanes in U.S. history, but this year marks a record eight hurricane-free seasons. No one seems to be enjoying this good fortune more than Florida property insurance carriers.

Despite escaping payment for hurricane claims for the last eight years and a 20 percent reduction in the cost of reinsurance this year, 69 percent of the rate requests that insurance companies filed with Florida Office of Insurance Regulation (OIR) were for rate increases.

State Farm, for one, hiked its rates by 6.3 percent in October although in the third quarter it reported $126 million in underwriting profits. State Farm says it uses its rate increases to purchase additional reinsurance. According to state regulators, Florida insurance companies must maintain all appropriate insolvency standards. Why continue to raise premiums to cushion reinsurance reserves that already exist instead of passing on savings to policyholders?

Florida’s Chief Financial Officer, Jeff Atwater, requested answers from state Insurance Commissioner, Kevin McCarty on why homeowner insurance rates have not seen a reduction, generally, when costs to insurance companies have gone down. McCarty’s report was due to be released on Dec. 18, but he asked for an extension until Jan. 15.

Not only are Floridians paying more in premiums when there have been no major storms, they are paying the highest rates in the country. A recent report by the National Associate of Insurance Commissioners (NAIC) showed that the average rate for a Florida homeowner’s insurance policy is $1,933. Louisiana is the second-highest, with an average $1,672. The national average rate is $978.

The NAIC’s annual report contains insurance rates from 2011, which was the most recent year with data available. Notably, the average rates do not reflect the more recent insurance increases Floridians faced in the last two years. The trend of state regulators consistently approving rate hikes does not show signs of slowing down.

Red Light Camera Tickets in Florida – Fair Game?

A notice appears in your mailbox. The envelope has a return address from New York or another random state. Inside the envelope is a traffic citation, with various color photographs of your vehicle breezing through a red light in a nearby town. Listed on the citation is your license plate number, date and time of the infraction, and most intrusively, a fine in the amount of $158.00. To top it off, the Notice provides thirty short days to pay the fine or to challenge the citation in a Florida court.

The first thing that runs through your mind is how is this even possible? Was I driving my vehicle on this particular date and on this particular time? Had I loaned my car to a spouse or to a friend? Why is New York citing me for a traffic infraction that allegedly occurred in Florida? Is any of this nonsense even lawful? The notice from New York seems to be legitimate.

Red light cameras are popping up all over Florida. Depending on your location in the State may determine if the citation is lawful. Specifically, the 5th District Court of Appeals (Orange, Seminole and surrounding counties) held that the City of Orlando does not have the specific authority under Florida Statute to impose such penalties. Specifically, the 5th DCA held that the imposition of additional penalties, over and above those already imposed by Florida’s legislature, do not fall within the specific authority granted to municipalities by Florida’s Constitution.

Conversely, the 3rd District Court of Appeals (Miami-Dade and Monroe counties) held that City of Aventura does have the authority to impose penalties based on red light camera infractions. The 3rd DCA held that such penalties do not invalidate the legislative intent behind the uniform traffic laws and specifications set out by Florida’s Department of Transportation.

The Florida Supreme Court heard oral arguments in November and will presumably render a decision early in 2014 regarding the lawfulness of the red light citations. What does this mean for people who get these tickets in the meantime? First and foremost, there are valid and lawful ways to challenge these citations. Upon notice of one of these citations, immediately contact an experienced attorney in your area. Remember that you MUST decide within thirty days whether you are going to challenge the ticket or pay the fine.

Contact your friends at Cohen Battisti for a free consultation and an explanation of your rights.

Article written by Paul Zeniewicz, Esquire

Floridians Face Surging Rate Hikes in National Flood Insurance Program

The National Flood Insurance Program (NFIP), which is supervised by the Federal Emergency Management Agency, is set to increase premiums in 2014. The cost is steep for Florida, which holds 37 percent of the federal flood insurance program’s policies.

Homeowners who are renewing their insurance face skyrocketing premiums, up to 20 percent in communities like Pinellas County. he high premiums are a result of changes to the NFIP, being implemented by the Biggert-Waters Flood Insurance Reform Act.

With Florida having more coastline than any state, Floridians have more flood policies and pay more into the program. The flood insurance rate increases affect Florida home sales and other title transfers. Although Florida theoretically stands the highest chance of flooding, Hurricane Katrina and Superstorm Sandy led to more NFIP claims being made in other states than Florida. Not only does Florida have the highest number of subsidized flood insurance policies, it is the state with the highest exposure to pay into claims, at $475 billion. Texas and Louisiana have the second and third highest exposure, at $162 billion and $112 billion, respectively.

Courtesy of NRDC

Courtesy of NRDC

According to a recent report by the Center for Competitive Florida, which analyzes the changes in the NFIP, Superstorm Sandy claims were estimated at up to $15 billion. Comparatively, Florida had $407 million in Tropical Storm Isaac claims in 2012.

Another study, conducted by the Wharton Center for Risk Management and Decision Processes, compared the amount of claims paid to the amount of premiums collected and revealed that Florida paid $3.60 for every dollar NFIP paid in a flood claim anywhere. The study showed that 11 states received more in payouts than was paid in premiums by the states’ policyholders over the course of 30 years.

Currently, the NFIP is $24 billion in debt. Thus, Congress passed the Flood Insurance Reform Act. The goal of the reforms is to reduce the debt by eliminating subsidized rates on older homes that don’t represent the properties’ true flood risk, and make the program more stable. Previously, rate increases were capped at 10 percent, but some Floridians risk paying four or six times their current rate, or even more.

Florida legislators are attempting to get a delay or roll back of the new rates passed before the session closes for the year, but Congress has yet to agree to delay any changes to the implementation of the Biggert-Waters Flood Insurance Reform Act.

Universal Property and Casualty agrees to pay $1.2M Fine, End “Post-Claim Underwriting”

The days of Universal Property and Casualty Insurance Company’s now well-known “post-claim underwriting” practices, which led to many homeowner’s having their property damage claims denied or have their policies canceled, and without the required notice of cancellation, are over. The property insurance giant has agreed to implement corrective action, change its policies and procedures and pay the $1.26 million fine ordered by Florida’s Office of Insurance Regulation.

This insurance company’s unjust denial of claims and cancellation of policies due to improper handling of claims resulted in numerous consumer complaints that were eventually brought to the attention of Florida’s Insurance Consumer Advocate, who at the time was Robin Westcott. The Insurance Consumer Advocate worked with the Office of Insurance Regulation, the agency responsible for overseeing that insurance companies are following proper procedures, to investigate the complaints that consumers had against Universal. The investigation revealed that Universal had been using their customers’ credit history information as a basis to issue denials on property damage claims, well after the time when policy underwriting was completed.

Essentially, Universal had been issuing policies and collecting insurance premiums after only conducting a partial underwriting of insurance policies, and then waiting until a homeowner filed an insurance claim to finish the process. In many instances, Universal alleged that the reason a claim was denied or a policy cancelled is because during the claims handling process, was based on a misrepresentation made by a homeowner on an insurance application. This would include, for example, if homeowners did not disclose a prior lien or judgment on the insurance application. Such information is publicly accessible in county records, and easily obtainable by an insurance company during the original policy underwriting process.

In May 2013, the Office of Insurance Regulation issued an Order with its findings that Universal had unnecessarily caused delays in paying claims to their customers, as well as denied claims and cancelled policies following the improper “post-claim underwriting” practices and in violation of Florida Statutes. Insurers are required to return unearned insurance premiums to the policyholder within fifteen days of the policy cancellation, and are required to give the policyholder proper and timely notice of the cancellation

Universal was ordered to pay $1.26 million in administrative fines as a result of the investigation conducted. Initially Universal challenged the Prior Order, but in October 2013, it signed a Consent Order, and agreed to implement changes to its claims handling and underwriting practices, as well as pay the fine. Universal will review 262 claims it previously denied on the basis of application misrepresentations. After Citizens, Universal is the second-largest property insurer in Florida, with more than 542,000 policyholders.

See the Consent Order in full.

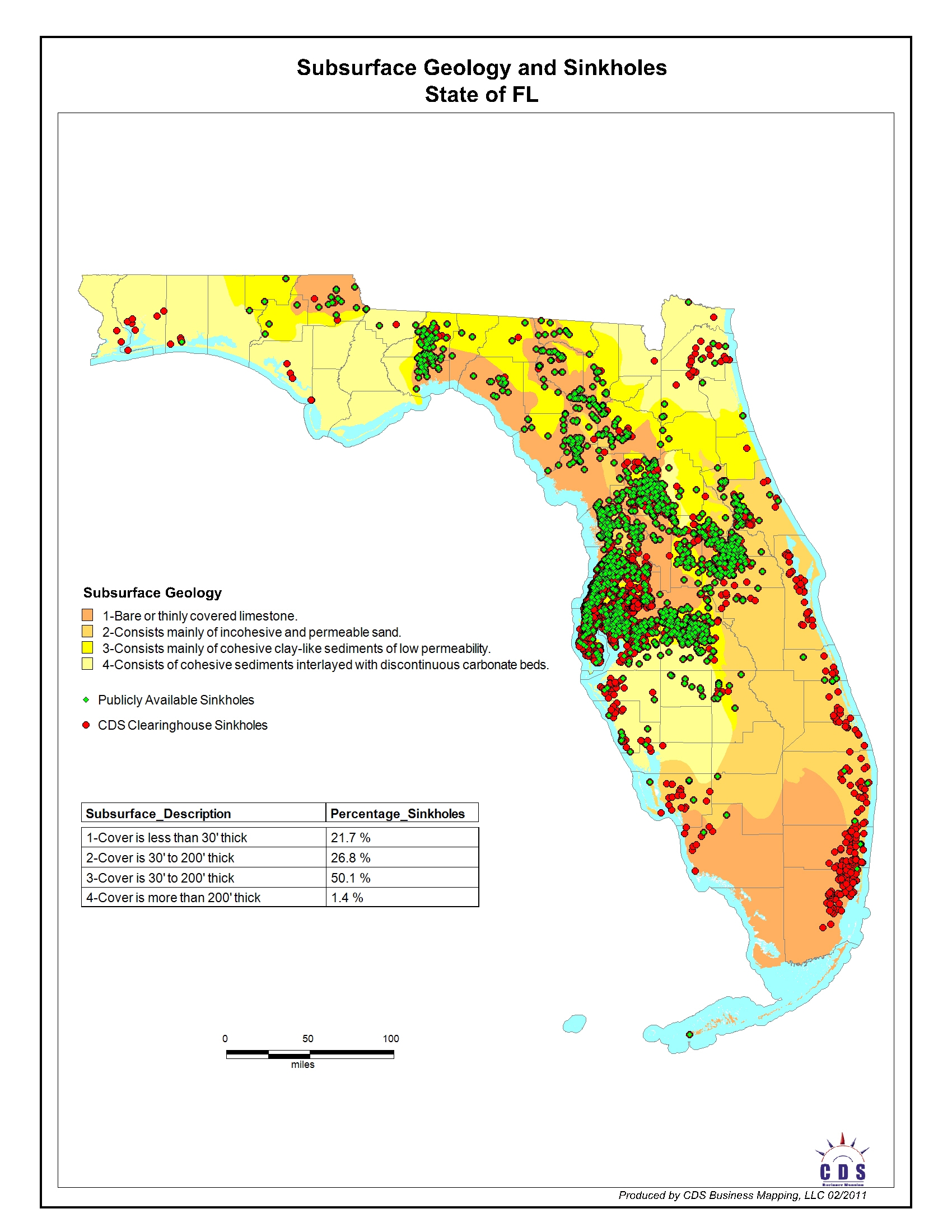

Citizens Changes Underwriting Guidelines to Include Sinkhole Properties

Citizens Property Insurance Corporation has recommenced issuing policies on homes with prior sinkhole claims. The new changes to Citizens’ underwriting guidelines, approved by the Florida Office of Insurance Regulation, now allow policies for properties that have had repairs from prior sinkhole damage.

The underwriting rules require that homeowners be able to prove, with documentation and photographs, that the sinkhole damage on their property has been repaired pursuant to recommendations from approved engineers. Homeowners who can show that their sinkhole damage has been partially repaired, or repaired using alternative methods can also still be covered under the new policies for some perils, but the new policies may not include coverage for a sinkhole in Florida.

Sinkholes form when limestone dissolves bedrock over time, and the surface land collapses. Depending on the circumstances, they can be filled with dirt, sand or concrete to support the foundation of a home. At one time, all Florida homeowner policies were required to have sinkhole coverage, but after years of insurance companies complaining that many sinkhole claims were fraudulent, and sinkhole claims tripling from 2006-2010, the Florida legislature passed a law limiting sinkhole coverage in 2011.

The new insurance coverage availability with Citizens, which went into effect on Oct. 31, is especially significant in Pasco and Hernando Counties, where real estate sales and property values sank in part because an estimated 20,000 properties were not insurable due to sinkhole risk. Homeowners with prior sinkhole claims did not qualify for property or storm coverage, even if the sinkhole damage was repaired.

Now, homeowners and potential buyers in the Tampa-area counties of Pasco, Hernando, Hillsborough and Pinellas, known collectively as “Sinkhole Alley”, can apply for mortgages that require insurance, when they previously would not qualify due to sinkhole damage.

The announcement for Citizens’ underwriting changes regarding sinkhole properties was made in New Port Richey, Fl. at a Nov. 20 meeting held by the Florida Association for Insurance Reform (FAIR) and the Pasco County and Hernando County Realtors. In the week before the announcement, two homes in Dunedin, located in Pinellas County, were swallowed by a 90-foot wide sinkhole, and residents in several nearby homes were evacuated until the sinkhole was determined to be stable enough to be filled.

Adult Literacy Spelling Bee

Author George R.R. Martin said, “A reader lives a thousand lives before he dies. The man who never reads lives only one.” While that is a powerful statement, did you know that only one in every five Central Florida adults reads at or below the fifth grade level? This is exactly what the Adult Literacy League is trying to change. This volunteer and donation based organization is attempting to change the world of those who have trouble reading “one page at a time.”

On October 24, 2013, The Adult Literacy League held an event they called “Lawyers for Literacy Spelling Bee” at the Doubletree by Hilton in Downtown Orlando. In this event was Cohen Battisti, Attorneys at Law’s own Michael Grossman! Not only did he do a fantastic job, but he was also very glad to be a part of such event. I had the chance to interview Mr. Grossman about the spelling bee.

CB: What do you think about the Adult Literacy League?

Michael Grossman: It’s really an amazing program being run by amazing people. Literacy is such an important skill, whether you’re looking for work, reading labels on food at the grocery store, or trying to read a bedtime story to your child. It’s easy to take for granted how important and necessary reading is in our day-to-day lives. For adults who are illiterate, whether because English is not their first language or they did not have the benefit of an early education, the Adult Literacy League is life-changing. I have the highest degree of respect for their volunteers and staff, this is an extremely noble cause that has a profound impact on our communities.

CB: How did you feel about being a part of the event?

Michael Grossman: It was an honor, but to be completely honest, also a little nerve-racking. When the Young Lawyers Section of the Orlando Bar Association contacted me the day before the event due to a last-minute cancellation, I was happy to fill-in but really nervous. After all, the other competitors had over a month to study the list of words to be used while I didn’t even recognize about 10% of the words on the list! Fortunately, the structure of the spelling bee meant I would not be alone, and was assigned a partner, Terri Spoon. Terri was an amazing speller and instrumental in our success.

CB: Did you struggle at any point, and what was the hardest word they had you spell?

Michael Grossman: The partnership between myself and Terri was really clutch. She was a tremendous help for any words with which I was struggling. I can’t remember all the words they gave us, but a couple tough ones that come to mind are vicissitude, precocious, and peccadillo.

CB: What place did you come in?

Michael Grossman: Winner, winner chicken dinner, we came in first place!

CB: Is this something that you would do again if you had the opportunity?

Michael Grossman: Without question. It was a fantastic event, Judge LeBlanc was an affable and charismatic MC, and everyone really had a great time helping a worthy cause.

It was great to have someone from Cohen Battiti, Attorneys at Law not only at the event, but to take first place in it! Keep that in mind the next time you are in need of legal attention.

At Cohen Battisti, initial consultations are always free and confidential. We have a very experience group of attorneys and legal staff ready to assist you with your needs! Call Cohen Battisti, Attorneys at Law today at 407-478-4878, or go to www.CohenBattisti.com. Remember, at Cohen Battisti, “It’s About Justice!”

Hurricane Sandy – One Year Later

Hurricane season 2013 continues to roll on. However, today’s date marks a tragic event in hurricane history. Today, October 29, 2013, is the one-year anniversary of Hurricane Sandy: the super storm the rocked the North East.

Not only were billions of dollars worth of damage and some 366,000 structures damaged during the storm, but an estimated 160 people in the United States lost their lives. Many more lost their homes. Today, there are still thousands of people who are still trying to get back to what they called home.

If you are in the restoration industry, you know it may be extremely difficult to get insurance companies to pay out during tragic events such as this. In the state of Florida, law firms such as Cohen Battisti, Attorneys at Law know this well, and are here to make sure that insurance companies pay you (the restoration company) for the work you’ve done.

The Huffington Post has a great article featuring interactive before (destruction) and after (reconstruction) pictures with a slider to go back and forth between the images. This is a screen shot of one of them.

Courtesy of the Huffington Post

Reports say that Hurricane Sandy was the deadliest US cyclone outside of the southern states since Hurricane Agnes of 1972. The National Hurricane Center said the Sandy ranks of the second-costliest tropical cyclone on record, after Hurricane Katrina of 2005.

Hurricanes cannot be prevented, but you can prepare for them. During hurricane season, always make sure that you have, and follow a hurricane checklist of some sort. If you are a restoration company, make sure you get paid for your work by using an Assignment of Benefits contract. Experienced law firms such as Cohen Battisti, Attorneys at Law are able to help you with this.

The North East took a hard hit, but they are getting back on their feet. The battle still isn’t over though.

{kind=link}